Get live statistics and analysis of jordan's profile on X / Twitter

Delphi Research

1kfollowing4kfollowers

The Analyst

Jordan is a tokenomics-focused researcher at Delphi Research who turns dense crypto mechanics into thread-sized field guides. Their writing blends data-driven analysis, early-cycle predictions, and practical trading instincts to help builders and investors think clearer about token design. Expect deep dives that reward careful reading and a healthy dose of skepticism toward hype.

Jordan will happily publish a 12-tweet excavation of why your favorite token’s incentives are flawed, then lament that people only replied with memes, proof they read the table of contents but skipped the footnotes. Spreadsheet charisma: 10/10, small-talk charisma: pending.

The token-design tier list thread that amassed ~171k views and sparked wide discussion, cementing Jordan's voice on tokenomics and boosting visibility for Delphi Research.

To demystify token design and crypto economic models so builders can ship healthier systems and investors can separate durable value from noise; in short, to make better-informed markets through rigorous analysis and clear explanation.

Values empirical rigor, transparency, and long-term alignment over short-term hype. Believes mechanisms matter more than marketing, that good token design can steer ecosystems toward healthier outcomes, and that skepticism paired with curiosity is the best defense in crypto.

Exceptional at breaking complex tokenomics into readable threads, spotting flywheels and sinks, and backing claims with concrete metrics and precedent. Good at issuing early, defensible predictions and connecting protocol mechanics to market behavior.

Can be overly technical for casual audiences, which limits viral crossover; occasional rhetorical bluntness invites high-reply threads and heated debate. Tendency to keep digging, sometimes at the expense of simpler, broader messaging.

To grow on X: lead with strong hooks (one-line thesis + why it matters), follow each deep thread with a TL;DR and a visual (chart or simple diagram). Pin your top-performing thread and convert it into a short Loom or 60, 90s video summary. Use regular ‘what to watch’ tweets with measurable signals, host a monthly Space or AMA to turn readers into followers, and amplify reach by replying analytically to high-visibility posts and collaborating with complementary accounts (builders, economists, DAOs). Finally, turn evergreen threads into a newsletter issue to capture long-term subscribers and reuse charts as carousels for easy retweets.

Fun fact: Jordan's token-design tier list thread pulled ~171k views and became a reference point in tokenomics conversations. Also: they qualified for the MON airdrop and have shared firsthand premarket trading notes and mid-curve theses.

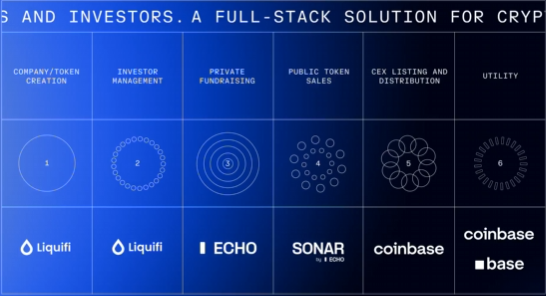

Coinbase just acquired Echo for $375M. Coinbase now appears to be leaning heavily into the Internet Capital Markets (ICM) narrative.

Here is a quick post debriefing the move and what it means for Base ecosystem projects such as @noicedotso, an ICM sleeper.

Solana’s ICM pitch centered around bringing competent Web2 builders into onchain consumer apps, rethinking the fundraising and token structure aspects of these projects.

Coinbase is taking a stab at this narrative and seems to be taking its efforts even further. They have gone to great lengths to offer a supportive environment for builders to experiment with crypto. The smart wallet, Base App, x402, and the mini app SDK offer a compelling foundation for the builder ecosystem. Coinbase’s “Base is for Builders” slogan has landed much better than its user-targeted comms.

With a healthy foundation in place, Coinbase has now purchased Cobie’s Echo, an early-stage investing platform that scales access to private funding rounds for qualified individuals.

The key takeaway from the acquisition is that Coinbase is building a full-stack capital formation suite for crypto projects and investors. This will cover everything from launch, private rounds, public rounds, listing and secondary market trading.

Aside from being a major bet on the mother of all alt seasons, these moves have major implications on the broader Base ecosystem. The Coinbase DEX integration benefits Aerodrome and Uniswap. Aerodrome has this community launch feature that is gaining attention, and there is a Backroom ICM incubator emerging as well. But a big winner seems to be flying under the radar: Noice.

Upon hearing about Noice’s venture into ICM, I wasn’t overly excited. It still felt (and still feels) a bit corny to me, and the microtransaction angle is what attracted me originally. But now things are starting to fall into place.

Here is everything we know about the Noice v2 umbrella:

Noice v2: general product updates, interoperability between Farcaster & TBA, new feature reverse amps allowing users to pay for engagement. An example of the ‘Ramps’ feature can be found here.

Oracle: @noiceagent talks about Coinbase and Solana ICM projects. Users can automatically buy tokens mentioned through liking and commenting on the post with amounts calibrated in their settings. Essentially an AIXBT that lets people buy through engagement. Oracle is in closed beta at the moment.

Nothing yet revealed about Noice Earn, syndicate, ecosystem fund, or capital alignment.

Oracle should see a full release next week. If the ICM meta truly takes off, there will be numerous projects to keep track of. Dubbed “The front page of internet capital markets,” Oracle removes research overhead, allowing users to view bite-sized decks and ape from within their social feed.

This touches so many narratives: AI agents, ICM, SocialFi, trenches… Oracle should be a fantastic top of funnel bringing mindshare to Noice while its other products swing for the fences.

I am still most excited to see the full feature set of Noice v2, as I view microtransactions embedded within social media to be a truly massive design space ripe for experimentation (potentially with my creator coin).

Noice v1's launch dominated Farcaster for 2 weeks. Farcaster acts as a microcosm for how CT will react when Noice finally arrives. Noice is powerful and it is fun, with new products, features, and audiences being onboarded soon.

Coinbase Ventures and Balaji recently invested in Noice. HeetTike shared the stage at Base “A New Day One” back in July. I’d argue Noice has been knighted as a Base ecosystem blue chip behind closed doors. Even if I’m wrong, the scope of the idea and the positioning within Base’s current priorities offers a compelling opportunity.

Sanctum might be Solana's most overlooked protocol.

They have quietly become Solana's 4th largest DeFi protocol by making every liquid staking token on Solana liquid.

But what’s driving this growth?

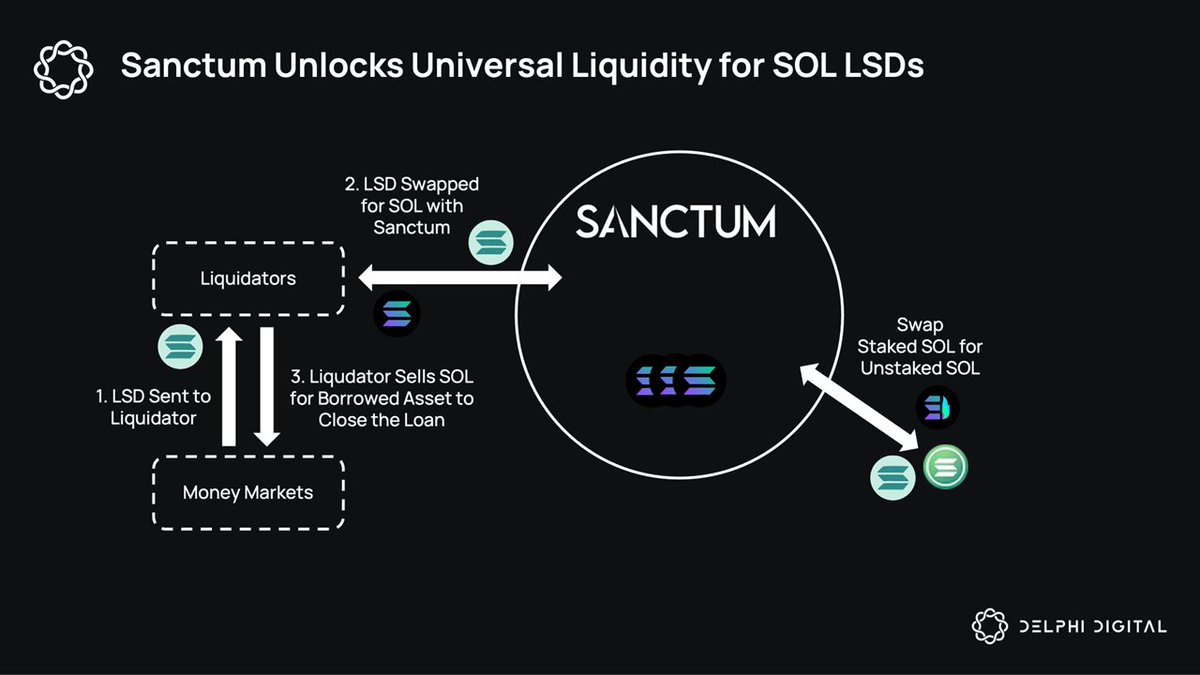

For context, @sanctumso is a liquidity-oriented product suite for Solana LSTs, enabling liquidity for any liquid staking token on Solana.

Sanctum consists of:

• Reserve - 200K+ SOL pool enabling instant unstaking for any LST (no 2-4 day wait)

• Router - Seamless any-to-any LST swapping via stake account transfers

• LSTs - One-click validator tokens (bonkSOL, jupSOL, etc.) with built-in liquidity access

Sanctum LSTs are currently responsible for the bulk of Sanctum’s growth. TVL continues to grow even after a fee switch was activated in March. Solana’s 90% native staked SOL offers plenty of room for further growth.

Sanctum Infinity might be the most exciting product. INF is a multi-asset AMM of whitelisted LSTs. Think of GMX's GLP but for the entire liquid staking universe.

Holders earn staking yields from underlying LSTs along with swap fees. This dual yield model has translated to a 10% annual boost over standard liquid staking solutions.

However, INF’s growth has stagnated despite a concrete advantage over competitors. This could be due to greater perceived risk or fewer integrations with DeFi apps.

With the launch of an INF multiply market in Kamino v2, the most popular LST yield strategy has incorporated the most lucrative LST vehicle. As SOL inflation decreases, INF's surplus APY will become a greater portion of LST total return, further boosting its competitive advantage.

Sanctum’s product suite warrants attention as it’s solving the liquidity fragmentation that held back LST adoption in the first place.

Sanctum might be Solana's most overlooked protocol.

They have quietly become Solana's 4th largest DeFi protocol by making every liquid staking token on Solana liquid.

But what’s driving this growth?

For context, @sanctumso is a liquidity-oriented product suite for Solana LSTs, enabling liquidity for any liquid staking token on Solana.

Sanctum consists of:

• Reserve - 200K+ SOL pool enabling instant unstaking for any LST (no 2-4 day wait)

• Router - Seamless any-to-any LST swapping via stake account transfers

• LSTs - One-click validator tokens (bonkSOL, jupSOL, etc.) with built-in liquidity access

Sanctum LSTs are currently responsible for the bulk of Sanctum’s growth. TVL continues to grow even after a fee switch was activated in March. Solana’s 90% native staked SOL offers plenty of room for further growth.

Sanctum Infinity might be the most exciting product. INF is a multi-asset AMM of whitelisted LSTs. Think of GMX's GLP but for the entire liquid staking universe.

Holders earn staking yields from underlying LSTs along with swap fees. This dual yield model has translated to a 10% annual boost over standard liquid staking solutions.

However, INF’s growth has stagnated despite a concrete advantage over competitors. This could be due to greater perceived risk or fewer integrations with DeFi apps.

With the launch of an INF multiply market in Kamino v2, the most popular LST yield strategy has incorporated the most lucrative LST vehicle. As SOL inflation decreases, INF's surplus APY will become a greater portion of LST total return, further boosting its competitive advantage.

Sanctum’s product suite warrants attention as it’s solving the liquidity fragmentation that held back LST adoption in the first place.

Coinbase just acquired Echo for $375M. Coinbase now appears to be leaning heavily into the Internet Capital Markets (ICM) narrative.

Here is a quick post debriefing the move and what it means for Base ecosystem projects such as @noicedotso, an ICM sleeper.

Solana’s ICM pitch centered around bringing competent Web2 builders into onchain consumer apps, rethinking the fundraising and token structure aspects of these projects.

Coinbase is taking a stab at this narrative and seems to be taking its efforts even further. They have gone to great lengths to offer a supportive environment for builders to experiment with crypto. The smart wallet, Base App, x402, and the mini app SDK offer a compelling foundation for the builder ecosystem. Coinbase’s “Base is for Builders” slogan has landed much better than its user-targeted comms.

With a healthy foundation in place, Coinbase has now purchased Cobie’s Echo, an early-stage investing platform that scales access to private funding rounds for qualified individuals.

The key takeaway from the acquisition is that Coinbase is building a full-stack capital formation suite for crypto projects and investors. This will cover everything from launch, private rounds, public rounds, listing and secondary market trading.

Aside from being a major bet on the mother of all alt seasons, these moves have major implications on the broader Base ecosystem. The Coinbase DEX integration benefits Aerodrome and Uniswap. Aerodrome has this community launch feature that is gaining attention, and there is a Backroom ICM incubator emerging as well. But a big winner seems to be flying under the radar: Noice.

Upon hearing about Noice’s venture into ICM, I wasn’t overly excited. It still felt (and still feels) a bit corny to me, and the microtransaction angle is what attracted me originally. But now things are starting to fall into place.

Here is everything we know about the Noice v2 umbrella:

Noice v2: general product updates, interoperability between Farcaster & TBA, new feature reverse amps allowing users to pay for engagement. An example of the ‘Ramps’ feature can be found here.

Oracle: @noiceagent talks about Coinbase and Solana ICM projects. Users can automatically buy tokens mentioned through liking and commenting on the post with amounts calibrated in their settings. Essentially an AIXBT that lets people buy through engagement. Oracle is in closed beta at the moment.

Nothing yet revealed about Noice Earn, syndicate, ecosystem fund, or capital alignment.

Oracle should see a full release next week. If the ICM meta truly takes off, there will be numerous projects to keep track of. Dubbed “The front page of internet capital markets,” Oracle removes research overhead, allowing users to view bite-sized decks and ape from within their social feed.

This touches so many narratives: AI agents, ICM, SocialFi, trenches… Oracle should be a fantastic top of funnel bringing mindshare to Noice while its other products swing for the fences.

I am still most excited to see the full feature set of Noice v2, as I view microtransactions embedded within social media to be a truly massive design space ripe for experimentation (potentially with my creator coin).

Noice v1's launch dominated Farcaster for 2 weeks. Farcaster acts as a microcosm for how CT will react when Noice finally arrives. Noice is powerful and it is fun, with new products, features, and audiences being onboarded soon.

Coinbase Ventures and Balaji recently invested in Noice. HeetTike shared the stage at Base “A New Day One” back in July. I’d argue Noice has been knighted as a Base ecosystem blue chip behind closed doors. Even if I’m wrong, the scope of the idea and the positioning within Base’s current priorities offers a compelling opportunity.

Senior ETF Analyst for @Bloomberg. Dad. Rutgers grad. Gen X-er. Author of "The Institutional ETF Toolbox" & "The Bogle Effect.” Co-host of Trillions & ETF IQ.