Get live statistics and analysis of Value Maverick's profile on X / Twitter

I ask questions not to deny but to understand.

1kfollowing2kfollowers

The Analyst

Value Maverick is a meticulous and insightful thinker who dives deep into company fundamentals and market dynamics. With an impressive tweet count and a data-driven approach, they seek to understand the intricate details behind market movements rather than just hype. Their feed is a goldmine for thoughtful investors craving thorough and rational analysis.

Value Maverick, the human financial encyclopedia, who tweets so much you’d swear they’re trying to replace the entire SEC’s research team—but somehow still can’t explain why their following remains a closely guarded secret.

Successfully cultivated a dedicated community of investors who rely on their deep-dive analyses for making informed decisions, especially around stocks like $PLCE and $BYON, proving that patience and rigor trump hype.

To demystify the complexities of financial markets by providing clear, evidence-based investment insights that empower followers to make smarter, long-term decisions.

Value Maverick believes in the power of deep inquiry and rigorous data assessment over superficial trends. They value transparency, patience, and long-term thinking in investing, rejecting hype and focusing on substance.

Their greatest strength lies in thorough fundamental analysis and the ability to break down complex business models into digestible insights. Their consistent, high-volume content demonstrates dedication and expertise that builds trust.

Sometimes their deep dives may overwhelm casual followers who prefer quicker, snackable insights. Additionally, their heavy focus on data over emotional storytelling might limit broader viral appeal.

To grow their audience on X, Value Maverick should complement detailed threads with concise takeaway tweets that highlight key points for quick consumption. Engaging more in conversations, polls, and timely market news reactions will increase visibility and attract followers who value expert analysis but appreciate brevity.

Despite a lack of follower count data, Value Maverick engages heavily with 11,593 tweets, indicating a relentless commitment to sharing detailed analyses and fostering informed discussions.

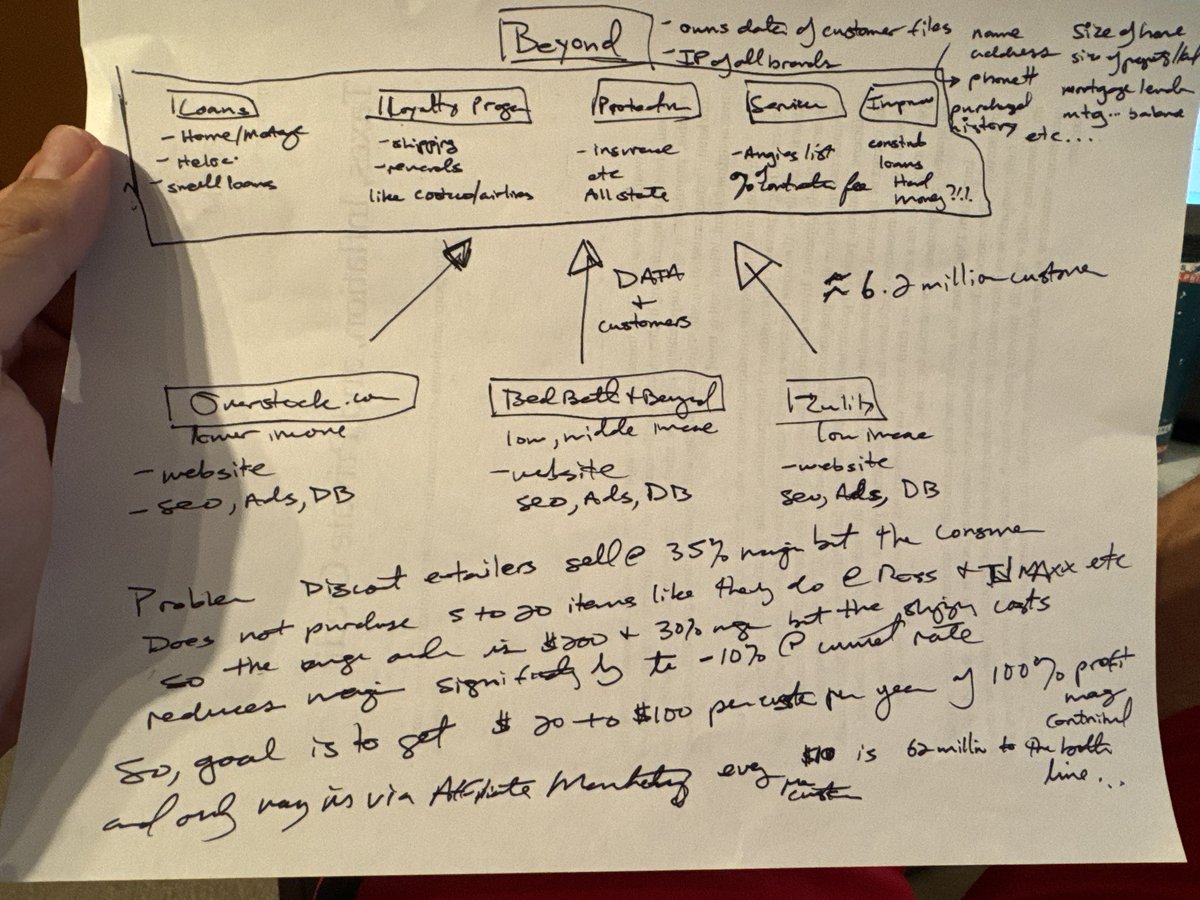

Been going deep into the $byon Piper call with @marcuslemonis which is the best call that lets you understand the future of the company. Here are a few bullet point points.

1. Traditional ecommerce and discount ecommerce is broken and will be hard to make money.

2. Bbb overstock and zulily attract specific demographics. Low income to upper middle income shoppers, mostly women. Has 6.2nm customers can easily get that to 10 to 20mm over time.

3. Data collected from the customers that purchase products will be used to sell other services. Like 5 to 10 other services and if each customer just buys $10 worth a year that is $62mm down to bottom line.

4. $byon is really going to be an affiliate business maybe hybrid membership business ala costco. Margins are 90% for this or higher. To really make the loyalty or membership program work they need to partner with a gas station and grocery chain, that will accelerate memberships and data IMO. Like wawa and kroger or publix etc. those locations can 1 to 2x a week frequency vs overstock which is maybe 2x a year frequency.

5. Business will be asset light so inventories will be very low. Capital will be spent in acquiring customers.

6. Wallstreet is valuing this as a traditional ecommerce business but if the plan works it will be modeled like a fin tech company like a SOFI. The analysts covering this will change, will have to.

Lots of risks and uncertainty if this will work. But if it does. It isna deca billion dollar company within 5 to 10 years.

Here is more or less an illustration. My handwriting sucks.

Been going deep into the $byon Piper call with @marcuslemonis which is the best call that lets you understand the future of the company. Here are a few bullet point points.

1. Traditional ecommerce and discount ecommerce is broken and will be hard to make money.

2. Bbb overstock and zulily attract specific demographics. Low income to upper middle income shoppers, mostly women. Has 6.2nm customers can easily get that to 10 to 20mm over time.

3. Data collected from the customers that purchase products will be used to sell other services. Like 5 to 10 other services and if each customer just buys $10 worth a year that is $62mm down to bottom line.

4. $byon is really going to be an affiliate business maybe hybrid membership business ala costco. Margins are 90% for this or higher. To really make the loyalty or membership program work they need to partner with a gas station and grocery chain, that will accelerate memberships and data IMO. Like wawa and kroger or publix etc. those locations can 1 to 2x a week frequency vs overstock which is maybe 2x a year frequency.

5. Business will be asset light so inventories will be very low. Capital will be spent in acquiring customers.

6. Wallstreet is valuing this as a traditional ecommerce business but if the plan works it will be modeled like a fin tech company like a SOFI. The analysts covering this will change, will have to.

Lots of risks and uncertainty if this will work. But if it does. It isna deca billion dollar company within 5 to 10 years.

Here is more or less an illustration. My handwriting sucks.