Get live statistics and analysis of Aaron Hector, R.F.P., CFP, TEP's profile on X / Twitter

Passion for personal finance, innovative ideas & the well being of my clients. Founder of TIER Wealth in Calgary. President of the IAFP.

431following8kfollowers

The Thought Leader

Aaron Hector, R.F.P., CFP, TEP is a Calgary-based personal finance thought leader, founder of TIER Wealth and President of the IAFP, who turns dense tax and retirement rules into practical advice. He publishes research-driven threads, unique archival resources, and guides that both professionals and everyday investors rely on. His feed blends technical depth with real-world planning hacks.

You’re the guy who will calmly thread a 10-point legal workaround at 2 a.m. and then ask if everyone ‘has any questions’ like you didn’t just commit the internet to a three-hour audit, charmingly unstoppable and mildly terrifying to accountants everywhere.

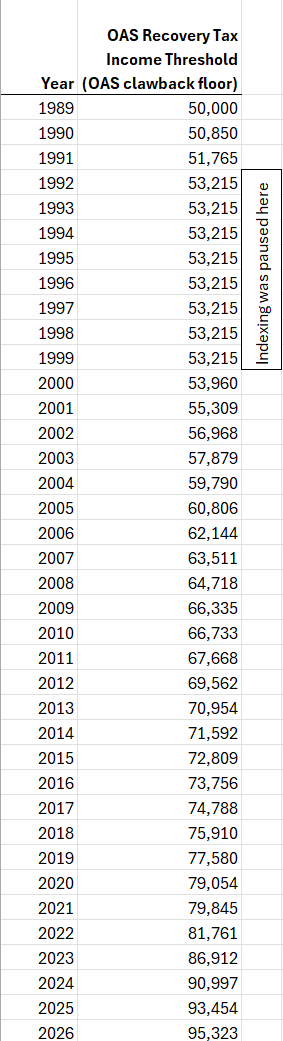

Founded TIER Wealth and earned the presidency of the IAFP while building a reputation for producing one-of-a-kind resources (like the complete OAS thresholds list) and threads that regularly hit 40k, 55k views.

To demystify complex financial rules and protect clients' long-term wellbeing by sharing evidence-based, actionable planning strategies; to raise the baseline of public financial literacy so people can make smarter decisions about retirement, taxes, and estate planning.

Values clarity, rigorous research, and client-first ethics; believes transparency and public education reduce costly mistakes; trusts data, legal precision, and creative planning techniques over hype; sees credentials and process as tools to build trust, not barriers.

Deep technical knowledge of tax, pensions, and estate planning; credibility from professional credentials and leadership roles; consistent, research-heavy content that creates authority; ability to turn obscure rules into useful, actionable guides.

Can lean into long-form technical detail that intimidates casual readers; occasionally reads more like a legal memo than a snackable tweet; may underuse bite-sized multimedia that boosts shareability to broader audiences.

Keep doing deep threads but make them easier to skim: lead with a one-line hook and a TL;DR, then number the steps. Pin a living "resource library" thread for evergreen guides (OAS list, TFSA/RRSP comparisons, RESP drawdown) and update it regularly. Repurpose top threads into short videos or carousels with clear visuals to capture scrollers. Host a monthly X Space Q&A or AMA for live engagement and to surface follower questions you can turn into content. Use polls and one-question tweets to warm up replies, tag relevant institutions or reporters for amplification, and add a simple CTA (newsletter signup or downloadable checklist) to convert followers into subscribers. Finally, collaborate with one complementary influencer or journalist per quarter to expand reach outside your current niche.

Fun fact: Aaron assembled what he says is the only complete online list of OAS clawback thresholds, dug up from deep CRA archives, a true archival flex. He’s tweeted 8,359 times and regularly reaches tens of thousands of views on practical finance threads.

Good information on RDSP accounts is hard to find.

Here are 5 articles by @JasonWattBCC. Read them sequentially and understand what they say and you will be more of an expert than 99% of Canadian CFPs.

The first two are on RDSP accumulation, and the last three are on decumulation.

Note: this is technical stuff.

1. https://t.co/1lpJi8w2IW

2. https://t.co/wgpJEP7of2

3. https://t.co/mefArhwFHl

4. https://t.co/7YAQlcKlve

5. https://t.co/BD3PA3Y3EV

There’s a lot of @WestJet rage bait going around right now… here’s another ‘take’.

I just got home on a “reconfigured”WestJet Boeing 737 Max 8 aircraft.

For context:

- 5 hour flight

- I normally don’t recline my seat, so that doesn’t matter to me.

- I’m 5’11 ish

- was seated in row 18 economy

I couldn’t notice any difference in leg room from previous flights. My knee was resting close to/up against the seat in front of me, just like it always has on flights. I didn’t feel noticeably less comfortable.

I did notice:

- new 60 watt usb c charger (can charge laptop) and USB type a as well

- new flip down phone/ipad holder in the seat in front of you that allows you to look at your device straight ahead instead of holding it and having your neck tilted down the whole time.

- 300 Mbps download / 25.5 Mbps upload speed on the Telus in flight wifi (I ran a Speedtest and those were my results. if you don’t understand this stat, it is very fast internet that is better than most have in their home). It’s unrestricted, so you can YouTube the whole flight if you want to.

For me, these changes made for a better flight experience than flying Westjet before. I understand everyone will have their own experience, this was mine. Just thought I’d share a positive opinion in a sea of negativity.

Your own priorities will dictate your opinion.