Get live statistics and analysis of Hedgie's profile on X / Twitter

🦔 Making financial nonsense make sense, one prickly take at a time 🦔 | Weekly newsletter: hedgie.markets | Not financial advice (I'm a Hedgehog)

21following17kfollowers

The Analyst

Hedgie is a razor-sharp financial analyst who turns complex, thorny economic realities into understandable insights, especially in the emerging AI and tech infrastructure spaces. Their witty, prickly takes cut through the hype to reveal the hidden risks lurking beneath surface-level optimism. With a dedication to data-driven truth, Hedgie educates and warns audiences about the financial engineering masking systemic vulnerabilities.

Hedgie’s idea of a fun day is probably arguing with investors about balance sheets while the rest of us just scroll past, eyes glazed over. They’re the kind of person who turns at parties to debug your financial assumptions—because who doesn’t want a hedgehog poking holes in your dreams right when you’re about to relax?

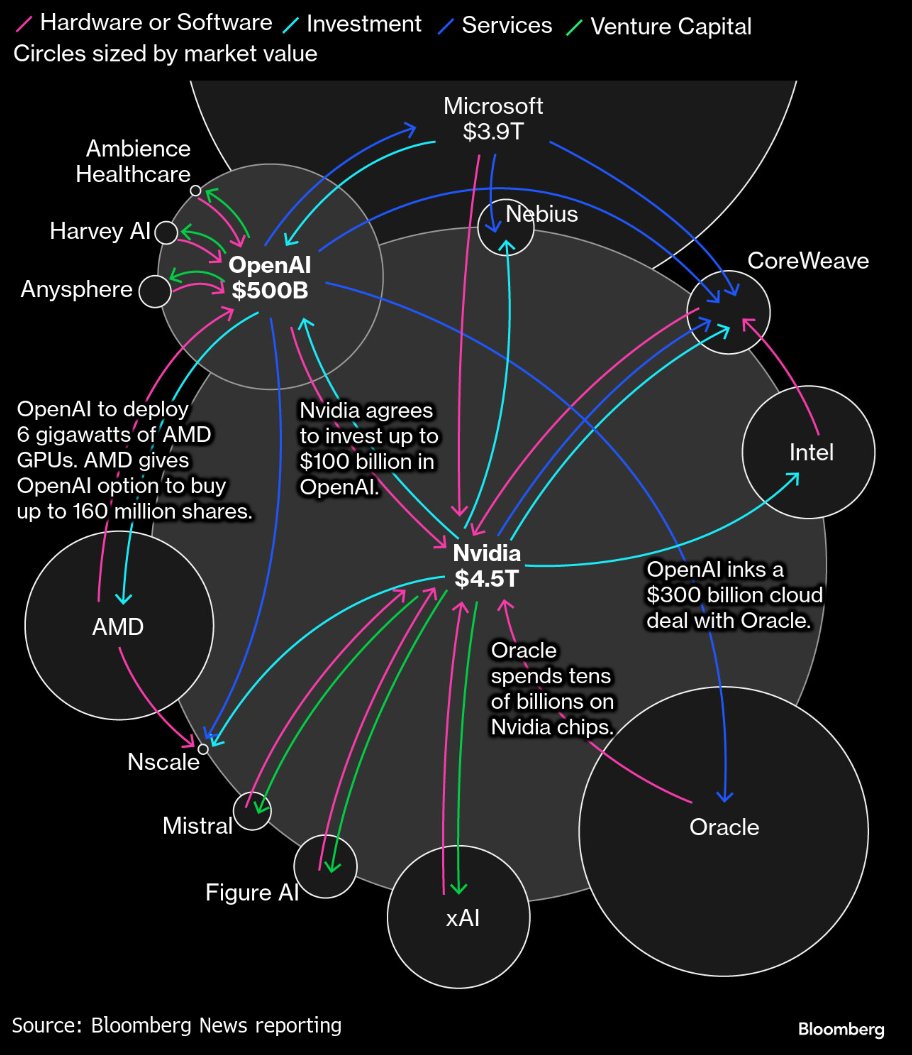

Breaking down Meta’s $30 billion off-balance-sheet AI infrastructure debt and connecting it to historic financial collapses grabbed massive attention, peaking at over 1.8 million views and sparking widespread discussion on the hidden risks of AI financing.

To expose financial illusions and educate audiences by decoding complex economic and technological ecosystems, helping people understand where real value lies versus speculative bubbles. Hedgie’s mission is to foster informed skepticism and promote transparency in finance and emerging technology.

Hedgie believes in rigorous analysis over hype and demands accountability from tech giants. They value transparency, intellectual honesty, and the power of data to challenge mainstream narratives. They also hold a healthy skepticism toward circular financing, inflated valuations, and the dangers of hidden economic risks.

Hedgie’s greatest strength is an exceptional ability to synthesize vast, complex financial data and market signals into clear, engaging narratives that expose systemic risks and bubble dynamics few dare to publicly discuss.

Their strongly critical and data-heavy style can sometimes alienate casual readers or those more inclined to optimistic tech hype, potentially limiting broader appeal. Also, the dense nature of their insights demands high engagement levels, which can be a barrier for quick social media consumption.

To grow their audience on X, Hedgie should consider integrating more bite-sized, visual summaries like infographics or short videos to complement their deep dives, making the content easier to absorb and share. Engaging directly with tech influencers and financial educators in threaded conversations can amplify reach and establish them as a go-to source in both finance and AI communities.

A fun fact: Hedgie’s tweets break down multibillion-dollar AI and tech finance deals with the precision of a hedge fund vet, all while embodying the personality of a hedgehog — prickly, resilient, and sharp-witted!